Executive Summary

The European Union’s emerging re-engagement with the People’s Republic of China (PRC), frequently characterised by policymakers as a pragmatic or transactional recalibration, constitutes a strategic misjudgement with compounding long-term risks.

While framed as a stabilising response to transatlantic uncertainty and a means of sustaining Europe’s green and industrial transitions, the empirical record demonstrates that this approach undermines European industrial resilience, entrenches asymmetric dependencies, and weakens the continent’s security posture. Rather than mitigating risk, the transactional pivot accelerates structural exposure across economic, technological, and security domains.

The Illusion of Strategic Balance

In January 2026, a recalibration of Western middle-power engagement with Beijing became increasingly explicit. UK Prime Minister Keir Starmer undertook the first visit by a British premier in eight years, securing limited trade concessions and visa liberalisation while arguing that Britain could not afford to disengage from the world’s second-largest economy. This logic was echoed at the January 2026 World Economic Forum in Davos, where Canadian Prime Minister Mark Carney defended a “third path” of pragmatic hedging, framing China less as a systemic challenger than as necessary economic ballast amid accelerating global volatility. Read our Strategic Assessment about “China’s Quiet Non-Wins at Davos”.

Image source: World Economic Forum (He Lifeng, Vice-Premier of the People’s Republic of China)

This momentum built on intensified European diplomatic engagement throughout late 2025. In December, Emmanuel Macron conducted a high-profile state visit to Beijing and Chengdu, signing more than sixty bilateral agreements across aviation, nuclear energy, and industrial cooperation. Macron framed France as a “power of balances”, advancing a multipolar vision intended to preserve European strategic autonomy through diversified partnerships rather than rigid bloc alignment.

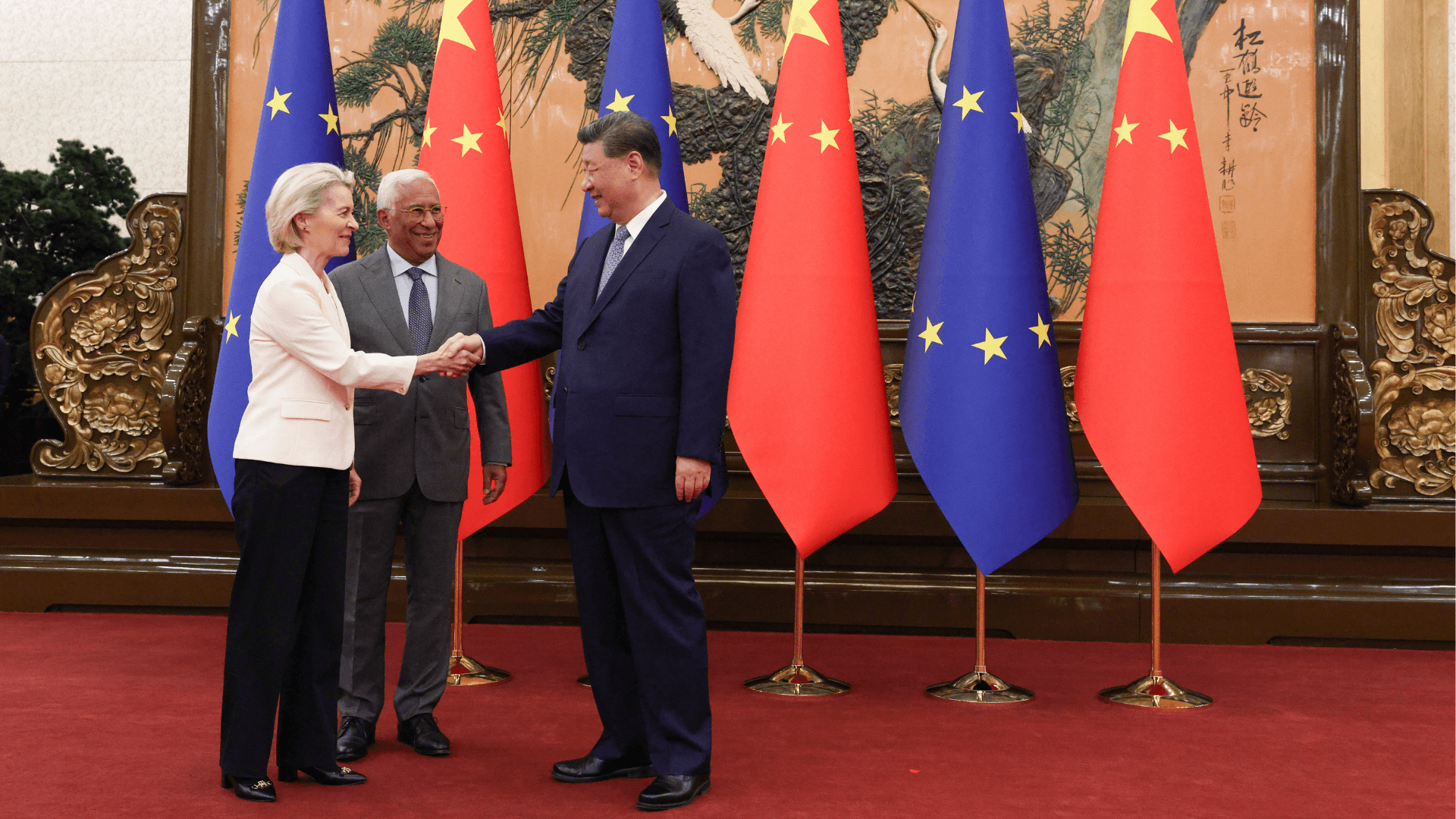

This posture was reinforced institutionally at the 25th EU-China Summit in July 2025, where Ursula von der Leyen and António Costa met with Premier Li Qiang and agreed to establish an “upgraded export supply mechanism” for rare earth elements. The initiative was publicly framed as a confidence-building measure to stabilise access to critical inputs for Europe’s green and digital transitions.

Parallel national efforts have followed a similar logic. Olaf Scholz has prioritised safeguarding Chinese market access for the German automotive sector, while Micheál Martin has positioned Ireland as a “bridge” for open trade with Beijing ahead of its 2026 EU Presidency, emphasising continuity and predictability in EU-China economic relations.

Taken together, these moves reflect a shared assumption: that engagement with the PRC can function as a stabilising counterweight to transatlantic volatility without imposing unacceptable strategic costs. However, this assumption rests on a misreading of both China’s internal economic trajectory and the structural asymmetry embedded in EU-PRC relations. Rather than restoring balance, the current diplomatic approach risks institutionalising a dependence that Beijing can selectively exploit, while limiting Europe’s strategic room for manoeuvre.

Systemic Hollowing

The economic rationale underpinning the transactional pivot is increasingly detached from empirical reality. European leaders frequently invoke the scale of the Chinese market and its presumed long-term growth potential as justification for deeper engagement. Yet audited fiscal and demographic indicators point to a structural slowdown rather than cyclical weakness.

By mid-2025, the PRC’s total debt-to-GDP ratio had reached 295.6%, which severely constrains fiscal flexibility across provincial and municipal governments. The prolonged downturn in the property sector – now entering its fourth year – has erased approximately US$18 trillion in household wealth, undermining consumer confidence and suppressing domestic demand. This contraction is not temporary. With household balance sheets impaired and local governments burdened by off-balance-sheet liabilities, the capacity of the Chinese economy to absorb European exports at scale has been alarmingly reduced.

Demographic trends reinforce this bleak outlook. China’s working-age population is shrinking by around 5 million people annually, while population ageing is accelerating at a pace that will see the PRC’s median age surpass that of the European Union by mid-century. These dynamics imply rising social expenditure, declining labour productivity growth, and a diminishing consumption base – conditions fundamentally incompatible with the role of a reliable external growth engine.

At the industrial level, the consequences for Europe are already measurable. The PRC’s “Dual Circulation” strategy has translated into sustained state-directed overinvestment in manufacturing capacity, with Chinese industrial investment growing by 9.5% in 2025 despite stagnant global demand. The resulting export glut has, in turn, systematically undercut European producers.

In electric vehicles, European Commission investigations confirm that Chinese manufacturers benefit from state support equivalent to roughly 20% of vehicle value, including subsidised energy and below-market lithium inputs. This has driven a rapid increase in Chinese EV market share in Europe from 5% to 28% in three years. In steel, exports reached an eight-year high of 90 million tonnes in 2025, priced approximately 20% below European production costs.

These patterns replicate the earlier experience of solar manufacturers, where sustained price dumping contributed to a 90% collapse in European production capacity over a decade. The cumulative effect is not competitive pressure but structural hollowing, as European firms face sustained losses, underinvestment, and eventual exit from strategically critical sectors.

Strategic Dependency

The transactional pivot carries implications that extend well beyond economics. Deepened engagement with Beijing is strategically incompatible with the EU’s stated security objectives, particularly in the context of Russia’s ongoing war against Ukraine.

Customs data from 2025 indicates that the PRC now accounts for 70% of Russia’s imports of high-priority dual-use components, including CNC (computer numerical control) machine tools and precision ball bearings essential for weapons production. Data released by the Kyiv School of Economics (KSE) and the Yermak-McFaul Working Group in 2025 indicates that China’s share of critical components in Russian drones and missiles has surged to approximately 70-80%.

Specifically, Ukrainian intelligence reported in mid-2025 that in newer Russian systems like the “Delta” drone, nearly every internal component – from the flight controllers and sensors to the engine – was of Chinese origin. This shift is a direct result of Russia’s “technological sovereignty” efforts failing, leading Moscow to swap sanctioned American chips from companies like Intel and Texas Instruments for Chinese alternatives, underscoring Beijing’s role as a de facto enabler of Russia’s war economy.

Physical security risks have escalated in parallel. Following the 2023 Balticconnector incident, 2025 recorded three separate cases of subsea data cables being severed by PRC-flagged vessels in the Baltic and North Seas. While individual incidents may be framed as accidental, their cumulative pattern aligns with a broader trend of strategic pressure on European critical infrastructure.

Dependency risks are most acute in critical raw materials. Until 2023, the PRC processed approximately 99% of global heavy rare earth elements, giving Beijing near-total control over essential inputs for defence, renewable energy, and advanced manufacturing. Since December 2023, export licensing requirements have expanded to graphite, gallium, germanium, and antimony.

Technology exposure compounds these vulnerabilities. European firms operating in China increasingly do so under joint-venture arrangements governed by the PRC’s National Anti-Espionage Law, which mandates local data storage and grants authorities potential access to source code. Emerging investigations suggest that similar dynamics are now unfolding in advanced medical technologies, including diagnostics and MRI systems, threatening some of Europe’s last remaining high-value manufacturing sectors.

Concluding Assessment

The cumulative evidence demonstrates that a transactional pivot toward the PRC produces industrial erosion, strategic vulnerability, and security incoherence. Rather than enhancing European strategic autonomy, it constrains it by embedding asymmetric dependencies that Beijing can exploit across economic, technological, and geopolitical domains.

A sustainable European strategy requires systematic de-risking rather than renewed engagement. This includes accelerated diversification of supply chains toward the Indo-Pacific and the Americas, strengthened foreign direct investment screening to block state-subsidised acquisitions, and the repatriation of critical manufacturing capacity under the 2025 European Industrial Act.

The strategic choice facing Europe is therefore not between engagement and isolation, but between absorbing manageable friction within a rule-based alliance system and locking itself into a dependency relationship with an actor whose interests are structurally misaligned with European stability. To respond to transatlantic strain by re-anchoring Europe’s future in Beijing should not be misconstrued as strategic balancing, but rather unambiguously interpreted as a self-inflicted weakening of Europe’s economic and security foundations.

Image source: European Council (Ursula von der Leyen, António Costa and Xi Jinping – Beijing, China – 24 July 2025 © European Union)