Two and a half years after it was announced during the 2023 G20 summit in New Delhi, the India-Middle East-Europe Economic Corridor is still one of the most ambitious infrastructure projects in the world. In practice, it remains a memorandum of understanding rather than a functional trade route. The events of the past years, including the wars in Gaza and Iran, have made the logic behind IMEC more evident, although they have complicated its execution. Understanding where the project genuinely stands, separate from the promotional language surrounding it, matters more today than at any point since its launch.

A Growing Geopolitical Necessity

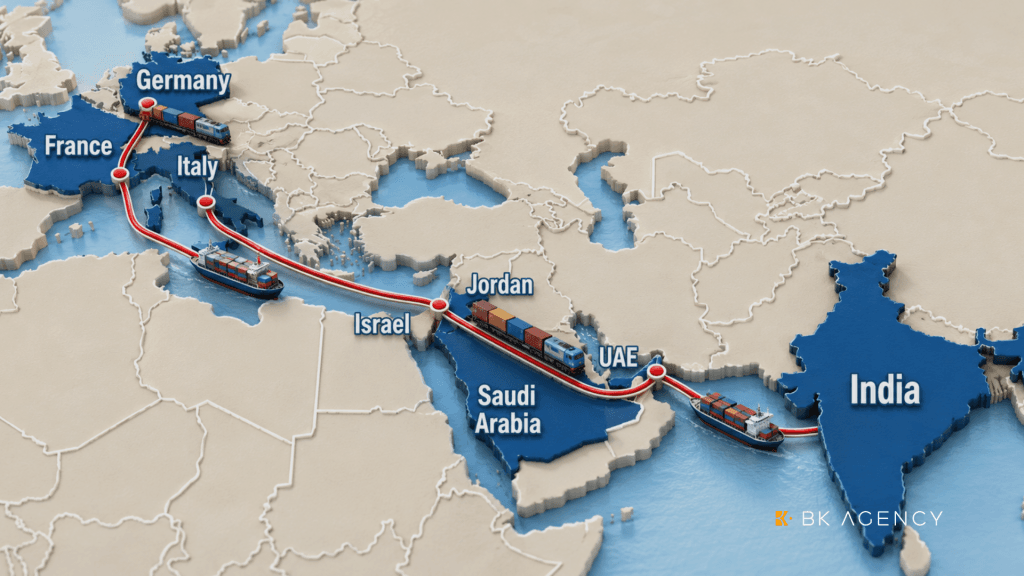

IMEC’s roots lie in a steady realignment across the Gulf and South Asia. India’s outreach to Gulf states in the 2000s, the 2020 Abraham Accords normalising ties between Israel and several Arab states, and the 2022 formation of the India-Israel-UAE-US grouping known as I2U2 together built the diplomatic basis that made a formal corridor announcement possible. In September 2023, India, the United States, the UAE, Saudi Arabia, the European Union, France, Germany and Italy signed a memorandum of understanding for a route that combines sea and rail transport with the eastern leg connecting Indian ports to the UAE, and a northern leg running by rail through Saudi Arabia and Jordan to Israel’s Mediterranean coast, before continuing by ship to Europe.

The original pitch centred on economic efficiency and geopolitics equally. Proponents claimed the route could cut shipping times to Europe by up to 40% compared with the Suez Canal, while offering India and Western countries a plausible alternative to China’s Belt and Road Initiative. Such a framing shifted after October 2023. The war in Gaza has worsened precisely the relationships between Israel and Arab states that IMEC depends, while the 2026 war in Iran and the subsequent blockade of the Strait of Hormuz delivered an even stronger argument for the corridor’s existence. Imports of energy and goods into Europe were shown to be overtly exposed to a single route that a hostile actor could close arbitrarily. IMEC’s appeal today rests specifically on offering a route that does not run through Iranian waters or depend on Tehran’s cooperation, on top of the proclaimed efficiency benefits.

The Starting Point

India’s interest in IMEC should not be regarded separately from the collapse of its main alternative. For twenty years, India has been developing Iran’s Chabahar port to create a trade route to Afghanistan and Central Asia that completely bypasses Pakistan. This port serves as the foundation for the larger International North-South Transport Corridor, which links India to Russia through Iranian territory. Washington revoked India’s sanctions waiver for Chabahar in September 2025, granted a short conditional extension, and let it lapse in April 2026 during the wider war with Iran. India has reportedly started to explore a temporary transfer of its stake in the port to an Iranian partner simply to preserve the option of returning later. With its Iran-based route uncertain and its overland access to Central Asia blocked by Pakistan, India’s remaining options to trade with the west narrow considerably. The options currently seem to be either a deeper reliance on China (which New Delhi is generally trying to avoid) or a route through the Gulf and the Mediterranean that excludes both Iran and Pakistan. IMEC is effectively the only alternative left standing.

IMEC arrives together with another related development for Brussels: the EU-India Free Trade Agreement. The negotiations between the parties concluded in January 2026 after nearly two decades of talks. Described by European and Indian officials as “the mother of all trade deals”, the agreement is supposed to eliminate tariffs on the majority of goods traded between two markets that together account for roughly a quarter of GDP globally. IMEC functions as the physical infrastructure that could make the trade agreement deliver on its promise easier – without a functioning corridor, preferential tariffs are not so effective if goods still need to travel through unstable routes. Brussels has framed IMEC as part of its broader Global Gateway strategy and positioned it explicitly as a transparent alternative to Chinese infrastructure lending in third world countries.

For the Gulf states, the corridor is a chance to diversify their economies away from oil, putting the UAE and Saudi Arabia on the map as logistics and energy hubs instead of pure energy exporters. As far as Washington is concerned, IMEC is one of the few concrete legacies of Gulf-Israel normalisation that could survive a difficult political period, giving the US a reason to keep the Abraham Accords framework functioning even as Saudi Arabia has made clear that full normalisation with Israel remains conditional on progress toward statehood of Palestine. Israel, for its part, has an obvious interest in a project that ties its own economic prospects to India, the Gulf and Europe, deepening the web of relationships that make regional isolation less likely.

The Europe’s Front Door

There is a considerable competition over IMEC’s European entry point. France has pushed Marseille, hosting its own IMEC summit in 2025 and appointing a dedicated envoy. Greece has promoted Piraeus and Thessaloniki. Italy has been having arguably the most intense campaign, positioning the northern Adriatic port of Trieste as the corridor’s natural gateway. Trieste’s case rests on several advantages – it is the northernmost port in the Mediterranean sea and has strong existing rail connections into central Europe. Italian officials, including a dedicated special envoy for IMEC, have argued that Trieste is best placed to transport Indian and Gulf trade directly into central and Eastern European markets that could be harder to reach from France or Greece. A series of dedicated summits held in Trieste through 2025 and 2026 have reinforced this pitch, and Italy’s own trade and investment ties with India add weight to the claim. Instead of just one port, the most likely scenario is for multiple European endpoints to coexist at the same time, with each one distributing goods to a different part of the continent.

Mapping Out the Road…

IMEC is still mostly a set of bilateral agreements and infrastructure announcements rather than a single operational corridor. There is no central coordinating authority or a binding timeline that all signatories have agreed to. Nevertheless, some concrete progress exists. India and the UAE signed an intergovernmental framework agreement in 2024 to streamline logistics and customs on the eastern leg, and construction on select rail and port components began in April following year. But the northern leg, which depends on stable rail and political cooperation across Saudi Arabia, Jordan and Israel, has not made much tangible progress, in large part because the diplomatic conditions that were supposed to be the basis for it (a settled Gaza war and warming ties between Israel and Gulf states) have worsened.

War-risk insurance premiums for shipping through the Gulf also remain high after the Iran conflict, and will likely stay that way until commercial operators see a ceasefire followed by a prolonged period of peace. None of the major US government financing tools have a clear mandate to fund IMEC specifically, leaving funding dependent on a patchwork of Gulf sovereign wealth, EU Global Gateway money and national investment pledges from India and European governments. The probability of IMEC becoming a fully realised, single continuous trade corridor within the next five years is relatively low. The probability of it continuing to develop unevenly, through the bilateral agreements, particularly the eastern maritime leg and European connections, is considerably higher.

… and the Crossroads Therein

The most likely path in the near term is bilateral. Individual segments, such as the India-UAE logistics agreement or Gulf hydrogen and data cable projects, continue advancing independently, giving the corridor substance in practice even without a formal governing body. This scenario would deliver benefits to businesses willing to engage segment by segment rather than waiting for a finished product.

A more optimistic (and a slightly less likely) scenario would see a genuine coordinating mechanism emerge, potentially through the G7 or G20 channels, alongside a durable Gaza settlement and some stabilisation in relations between Israel and other countries in the region. Under this path, the northern rail leg through Saudi Arabia and Jordan could move from concept to construction within a few years, insurance costs would fall as regional risk perceptions ease, and IMEC could begin to approach the transformative role its architects originally envisioned.

The pessimistic scenario involves the continuation regional instability and constant tension between Israel and Arab countries that makes the overland leg highly unlikely for years. In that case, IMEC would likely transform to a mainly maritime and bilateral initiative, useful for India-Gulf and India-Europe trade but without achieving the integrated rail bridge that distinguishes it from regular shipping routes. Given the current trajectory of regional politics, this scenario can’t be ruled out, though currently this seems to be the outcome with the lowest likelihood.

The Effects and the Bigger Picture

The corridor will not meaningfully change shipping routes or customs procedures in the next year or two. Businesses that change their logistics plans expecting the project to finish quickly could likely be disappointed. However, the more immediate opportunity lies elsewhere. When it gets ratified, the Free Trade Agreement between the EU and India will create new compliance and customs demands for Indian firms seeking to enter the EU market, as well as for European firms seeking to expand to India.

More broadly, IMEC’s slow and uneven progress means that businesses in shipping, rail logistics, energy and digital infrastructure should focus on the individual segments and not necessarily the corridor as a whole. The energy and digital pillars, including hydrogen hubs and the Blue Raman submarine cable project connecting India to Europe via the Gulf, are advancing on separate and sometimes faster timelines than the transportation that gets most of the political attention. For companies in these sectors, opportunities may appear even before the rail line linking the Gulf to the Mediterranean is complete.

IMEC’s significance for Europe is, among other things, the diplomatic and economic weight it adds to the EU-India relationship. Combined with the newly concluded free trade agreement, the corridor gives Brussels a solid answer to the question of how to diversify supply chains and strategic partnerships away from an overreliance on China without substituting one dependency for another. Whether the physical infrastructure is ever built to the fullest extent or not, the political project of positioning Delhi as a partner of comparable weight to Beijing, but one operating within a transparent framework, is already in progress. That particular shift in framing may prove more consequential for the Europeans in the near term than the concrete infrastructure projects that are envisioned by the IMEC economic corridor.